Blockchain technology has become a central concept in digital currencies and beyond. But what exactly is it, and why is it causing such a stir? What are blockchain technology advantages and disadvantages? Blockchain is a decentralized database that forms a continuous chain of record blocks.

This technology supports cryptocurrencies such as Bitcoin and Ethereum by providing a secure and immutable record of all transactions. This introduction provides you with the basic knowledge to better understand and categorize the following discussion about the blockchain technology advantages and disadvantages.

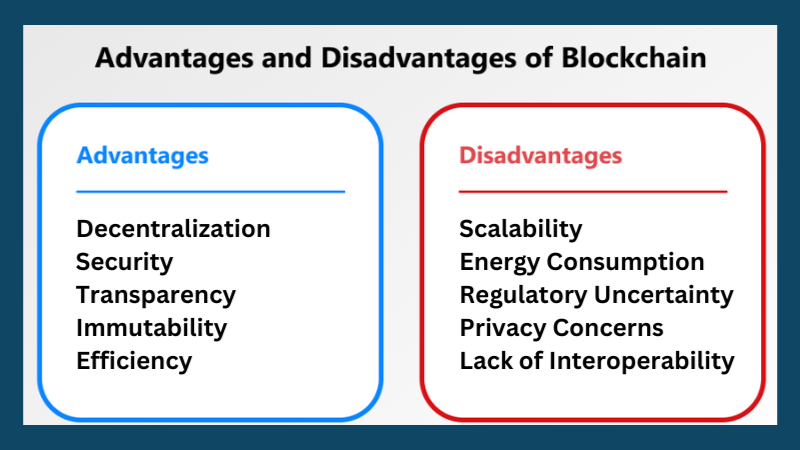

Advantages and Disadvantages of Blockchain Technology

Let’s take a closer look at the advantages and disadvantages of blockchain technology:

Blockchain Technology Benefits

1. Decentralization:

- It is the cornerstone of blockchain technology, providing a distributed network where no single entity has control. This removes the need for intermediaries, reducing the risk of censorship, manipulation, and single points of failure.

- Decentralization fosters trust among participants by ensuring that transactions are validated by consensus, rather than relying on a central authority.

- In applications such as finance, healthcare, and supply chain management, decentralization can improve efficiency, security, and trust by eliminating intermediaries and promoting peer-to-peer interactions.

2. Security:

- Blockchain employs cryptographic techniques such as hashing and digital signatures to secure transactions and data.

- Once a transaction is recorded on the blockchain, it is cryptographically linked to previous blocks, making it extremely difficult to alter without consensus from the network participants.

- The decentralized nature of blockchain also improves security by distributing data across multiple nodes, reducing the risk of a single point of failure or cyberattack.

3. Transparency:

- Transparency is a core feature of blockchain technology, as all transactions are recorded on a public ledger that is visible to all network participants.

- This transparency promotes accountability and trust, as participants can independently verify the integrity of transactions without relying on intermediaries.

- In industries such as supply chain management and food safety, blockchain transparency can enable consumers to track the journey of products from origin to destination, ensuring authenticity and ethical sourcing.

4. Immutability:

- Immutability ensures that once data is recorded on the blockchain, it cannot be easily altered or deleted.

- Blockchain’s feature enhances data integrity and trust, making it ideal for applications like land registries, identity verification, and intellectual property management, where preventing data tampering is crucial.

- However, it’s important to note that while blockchain data is immutable, the underlying systems and processes that interact with the blockchain may still be vulnerable to manipulation or errors.

5. Efficiency:

- Blockchain technology has the potential to streamline processes and reduce costs by removing intermediaries and automating tasks through smart contracts.

- Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automatically enforce and execute the terms of the contract when predefined conditions are met, eliminating the need for manual intervention and reducing the risk of errors or disputes.

- In finance, blockchain-based systems can facilitate faster and more cost-effective cross-border payments, trade settlements, and asset transfers by eliminating intermediaries and reducing transaction times and fees.

Disadvantages of Blockchain Technology

1. Scalability:

- Scalability refers to the ability of a blockchain network to handle increasing transaction volumes and maintain performance as the network grows.

- As blockchain networks grow, transaction validation may take longer and cost more due to increased congestion, resulting in slower processing times and higher fees.

- Scalability issues have been a significant barrier to widespread adoption of blockchain technology, particularly in applications requiring high throughput, such as payment processing and decentralized applications (DApps).

2. Energy Consumption:

- Many blockchain networks, particularly those based on proof-of-work (PoW) consensus mechanisms like Bitcoin and Ethereum, require significant computational power to validate transactions and secure the network.

- This energy-intensive process has raised concerns about the environmental impact of blockchain technology, as the mining of cryptocurrencies consumes large amounts of electricity, contributing to carbon emissions and climate change.

- Efforts are underway to develop more energy-efficient consensus mechanisms, such as proof-of-stake (PoS) and proof-of-authority (PoA), which consume less energy and offer potential solutions to the energy consumption problem.

3. Regulatory Uncertainty:

- The regulatory landscape surrounding blockchain technology and cryptocurrencies varies significantly from country to country and is still evolving.

- Regulatory uncertainty can create barriers to adoption and investment, as businesses and investors may be hesitant to engage with blockchain technology due to unclear or restrictive regulations.

- Governments around the world are grappling with how to regulate blockchain and cryptocurrencies, balancing the need to protect consumers and maintain financial stability with the desire to foster innovation and economic growth.

4. Privacy Concerns:

- Blockchain provides transparency and immutability, but it raises privacy concerns because all transactions are visible to all network participants.

- In applications where privacy is paramount, such as healthcare and personal finance, the transparent nature of blockchain may pose challenges in protecting sensitive information.

- Some blockchain platforms offer privacy features such as encryption, zero-knowledge proofs, and privacy-focused cryptocurrencies, but achieving a balance between privacy and transparency remains a challenge.

5. Lack of Interoperability:

- Interoperability refers to the ability of different blockchain networks to communicate and share data seamlessly.

- Currently, there are many different blockchain platforms and protocols, each with its own set of rules, standards, and interoperability challenges.

- Without interoperability between blockchain networks, communication and data sharing are limited, hindering widespread adoption and integration into existing systems.

- Efforts are in progress to establish standards and protocols for blockchain interoperability, aiding seamless interaction between different blockchain networks.

Understanding Blockchain: Basics and How it Works

To understand the basics and how blockchain technology works, it is important to first familiarize yourself with its structure. A blockchain consists of individual blocks that contain information such as transaction data and timestamps.

Each block has a unique hash value that identifies it, as well as the hash value of the previous block, which creates an unbreakable link.

The blockchain acts as shared record book where many participants (nodes) hold copies of the same data chain, ensuring transparency and reliability. If a new block is added, the network participants must validate it via a consensus mechanism.

This ensures the integrity and immutability of the entire chain. For cryptocurrencies like Bitcoin, mining involves performing complex calculations to create and verify new blocks in the blockchain.

A key feature of blockchain is that it enables real-time settlements without the need for a third-party intermediary.

This leads to a reduction in transaction costs and times. Encryption and decentralization boost security by eliminating weak points in traditional systems, reducing the chance of attacks or manipulation.

Conclusion: Blockchain Technology Advantages and Disadvantages

However, the strengths are also associated with weaknesses. High energy usage, scalability issues, application complexity, and legal uncertainties are significant concerns in blockchain technology. These factors represent significant hurdles that need to be overcome.

Considering the advantages and disadvantages of blockchain technology, it is up to companies, developers, regulators and legislators alike to set the course for the future of this technology.

Continuous dialog, training, and research, as well as exchange with all stakeholders, are essential for the maturation of blockchain and its successful integration into our digital society.

F.A.Q

- What is blockchain technology?

- Blockchain technology is a decentralized digital ledger system that records transactions across multiple computers in a secure and transparent manner. It forms a chain of blocks, each containing a unique record of transactions.

- How does blockchain ensure security?

- Blockchain employs cryptographic techniques to secure transactions and data. Each block is cryptographically linked to the previous one, making it difficult to alter or tamper with the data. Additionally, the decentralized nature of blockchain reduces the risk of a single point of failure.

- What are the advantages of blockchain technology?

- Some advantages of blockchain technology include decentralization, enhanced security, transparency, immutability, and efficiency. It eliminates the need for intermediaries, promotes trust among participants, and streamlines processes through features like smart contracts.

- Can blockchain be used beyond cryptocurrencies?

- ✅ Yes, blockchain technology has applications beyond cryptocurrencies. Blockchain is used in finance, healthcare, supply chain, and identity verification, boosting efficiency, security, and transparency.

- What are blockchain technology disadvantages?

- Disadvantages of blockchain technology include scalability issues, high energy consumption, regulatory uncertainty, privacy concerns, and limited interoperability between different networks. These challenges can limit its widespread adoption and effectiveness in certain applications.

- How does blockchain ensure transparency?

- Blockchain ensures transparency by recording all transactions on a public ledger that is visible to all network participants. This promotes accountability and trust as participants can independently verify the integrity of transactions.